Everyone is talking about the new tax bands. Your HR manager mentioned them. Your colleague said you might be paying less. Someone in a WhatsApp group posted a confusing screenshot about rates going from 0% to 25%.

But what does any of it actually mean for your salary?

This post explains Nigeria’s new 2026 PAYE tax bands in plain English. No accounting background needed. By the end, you will know exactly which bands apply to your income, how much tax each band takes, and why most salary earners in Nigeria are paying less in 2026 than they were in 2025.

New Tax Bands: What Are Tax Bands and Why Do They Exist?

A quick foundation before we get into the numbers.

Nigeria uses a progressive tax system. That means the more you earn, the higher percentage you pay. But here is the part that trips people up: you do not pay the higher rate on your entire income. You only pay it on the portion of your income that falls within that band.

Think of it like water filling a series of buckets. The first bucket fills up at 0%. The second bucket fills at 15%. The third at 18%. And so on. You only move to the next bucket after the one before it is completely full.

This is why two people can have very different tax bills even if they earn close amounts, and why someone earning N3.1 million does not suddenly pay 18% on their entire salary the moment they cross N3 million.

Key idea: The rate for each band only applies to the income that falls within that band, not your total income. This is called a marginal tax rate system.

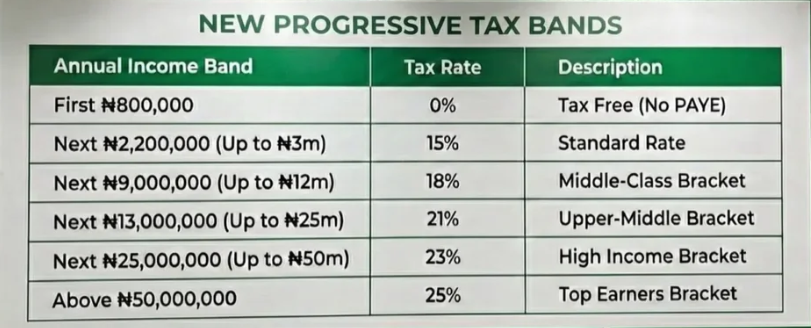

The Official 2026 PAYE Tax Bands Under NTA 2025

These are the bands that took effect on 1 January 2026 under the Nigeria Tax Act 2025.

| Annual Chargeable Income | Rate | Tax on This Band (Max) | Cumulative Tax So Far |

|---|---|---|---|

| First N800,000 | 0% | N0 | N0 |

| N800,001 to N3,000,000 | 15% | N330,000 | N330,000 |

| N3,000,001 to N12,000,000 | 18% | N1,620,000 | N1,950,000 |

| N12,000,001 to N25,000,000 | 21% | N2,730,000 | N4,680,000 |

| N25,000,001 to N50,000,000 | 23% | N5,750,000 | N10,430,000 |

| Above N50,000,000 | 25% | No cap | N10,430,000+ |

A few things worth noting about this table:

- The first N800,000 is completely tax-free. This is called the zero-rate band. Anyone whose annual chargeable income is N800,000 or less pays nothing. Not a reduced amount. Nothing.

- The bands build on each other. The cumulative tax column shows how much total tax a person has paid once their income has passed through all the bands up to that point.

- These rates apply to chargeable income, not gross salary. Chargeable income is what is left after you subtract pension, NHF, NHIS, rent relief, and other approved deductions from your gross pay. It is almost always lower than your gross salary, which is why your effective rate ends up lower than the headline band rates.

How the Bands Work in Practice: A Step-by-Step Example

Let us walk through a real salary and apply the bands one by one.

The scenario

Chisom earns N200,000 per month gross. That is N2,400,000 per year. Her employer deducts 8% pension (N192,000) and she is enrolled in NHF (N60,000 at 2.5%). No other deductions for now.

Step 1: Calculate her chargeable income.

Chargeable Income = N2,400,000 – N192,000 (pension) – N60,000 (NHF) = N2,148,000

But wait. Chisom also pays N840,000 in annual rent. The NTA 2025 gives her a rent relief of 20% of her actual rent, capped at N500,000.

Rent Relief = 20% x N840,000 = N168,000. This is under the N500,000 cap, so the full N168,000 is deductible.

So her final chargeable income is:

N2,148,000 – N168,000 = N1,980,000

Step 2: Apply the bands to N1,980,000

| Band | Taxable Amount in Band | Rate | Tax |

|---|---|---|---|

| First N800,000 (zero rate) | N800,000 | 0% | N0 |

| N800,001 to N2,016,000 (chargeable income) | N1,216,000 | 15% | N182,400 |

| Total | N2,016,000 | N182,400 |

Chisom pays N182,400 in tax annually. That is N15,200 per month. Her effective tax rate is N182,400 divided by N2,400,000, which comes to 7.6%.

Notice: although the 15% band applies to part of her income, she is not paying 15% of her total salary. The zero-rate band covered the first chunk. The 15% rate only touched the income above N800,000. Her overall effective rate is well below 15%.

How These Bands Compare to the Old PITA Law

The old bands are gone. Here is what replaced what.

| Feature | Old PITA | NTA 2025 | Who Benefits | Who Pays More |

|---|---|---|---|---|

| Tax-free threshold | N300,000 | N800,000 | Everyone | Nobody |

| Starting rate | 7% | 0% then 15% | Low earners most | Nobody |

| Top rate | 24% | 25% | N/A | Very high earners |

| Main housing relief | CRA: 20% of gross + N200k | Rent relief: 20% of rent, max N500k | Those who pay rent | High earners who claimed large CRA |

| Minimum individual tax | 1% of gross | Abolished | All salary earners | Nobody |

The most important change in the table above is the tax-free threshold jumping from N300,000 to N800,000. Under the old system, even the lowest earners started paying tax (at 7%) from their first naira of income above N300,000 after the CRA. Now that entire first chunk up to N800,000 is completely exempt.

The old CRA system (which gave you N200,000 plus 20% of gross income as a deduction before tax was calculated) was actually more generous for high earners. Someone earning N10 million annually got a CRA of roughly N2.2 million. Under the new system, they get rent relief of at most N500,000. That is why very high earners may pay slightly more under the new law despite the higher zero-rate band.

Quick Reference: Tax at Different Salary Levels

Here is how the bands play out across common Nigerian salary ranges. Figures assume 8% pension deduction only. Actual tax will be lower if you have additional deductions like NHF, NHIS, or rent relief.

| Monthly Gross | Annual Gross | Chargeable Income* | Annual Tax | Effective Rate |

|---|---|---|---|---|

| N60,000 | N720,000 | N662,400 | N0 | 0% |

| N100,000 | N1,200,000 | N1,104,000 | N45,600 | 3.8% |

| N150,000 | N1,800,000 | N1,656,000 | N128,400 | 7.1% |

| N300,000 | N3,600,000 | N3,312,000 | N378,960 | 10.5% |

| N500,000 | N6,000,000 | N5,520,000 | N726,600 | 12.1% |

| N1,000,000 | N12,000,000 | N11,040,000 | N2,107,200 | 17.6% |

| N2,000,000 | N24,000,000 | N22,080,000 | N4,843,800 | 20.2% |

* Chargeable income calculated after 8% pension deduction only. Add NHF (2.5%), NHIS, rent relief, or life insurance premiums to reduce this further.

Notice how the effective tax rate (the real percentage of your gross salary that goes to tax) is always significantly lower than the top marginal rate. This is the progressive system working as intended. The 18% band does not mean you pay 18% of everything.

Which Band Does Your Salary Fall In?

A simple way to think about this.

Your salary does not fall neatly into one band. It gets sliced across multiple bands as the income layers up. But if you want a rough sense of where the bulk of your income is being taxed, here is a practical guide:

- Earning N66,667/month or less (N800,000/year or less after deductions): You pay zero income tax. The entire chargeable income sits in the zero-rate band.

- Earning between N67,000 and N250,000/month: Most of your taxable income sits in the 15% band. Your effective rate will be well below 15% because the first N800,000 is still free.

- Earning between N250,000 and N1,000,000/month: Income starts spilling into the 18% band. Effective rate climbs but stays below 18%.

- Earning between N1,000,000 and N2,083,000/month: You are touching the 21% band. Still paying less than 21% overall.

- Earning above N4,166,000/month: The 25% top rate applies to income above N50 million annually. At N4.1 million monthly you are approaching but not quite there.

The only way to know your exact number with confidence is to run the actual calculation. That is what the NairaSeed Tax Calculator is for.

Common Misunderstandings About Tax Bands

“My salary crossed into the next band. Does all my income now get taxed at the higher rate?”

No. Only the portion above the band threshold gets taxed at the higher rate. If your chargeable income is N3,100,000, only N100,000 of that is taxed at 18%. The first N800,000 is still at 0%, and the N800,001 to N3,000,000 portion is still at 15%.

“I heard the top rate is 25%. Does that mean rich people pay 25% of everything?”

No. The 25% rate applies only to chargeable income above N50 million per year. Someone earning N60 million per year pays 25% on the N10 million that sits above the N50 million threshold. The first N50 million is still taxed at the lower bands below it.

“My payslip shows a tax rate of 12%. But the bands go from 0% to 25%. Which is right?”

Both. Your payslip is showing your effective tax rate, which is your total tax as a percentage of your gross salary. The 0% to 25% range refers to the marginal rates applied to each income slice. Your effective rate will always be lower than your marginal rate because the lower bands and the zero-rate band bring the overall average down.

“Do these bands reset every month or are they calculated annually?”

The bands are annual. Your employer calculates your PAYE monthly by dividing the annual tax liability by 12. So each month you pay one-twelfth of what your annual tax bill would be, based on your current gross income annualised. This is standard PAYE practice.

See exactly which bands your salary touches.

The NairaSeed Tax Calculator shows you a band-by-band breakdown of your 2026 PAYE. Enter your salary and deductions and see exactly how much tax lands in each bracket, your effective rate, your monthly net pay, and a comparison with the old law. No guesswork.

>> Calculate your band-by-band 2026 tax breakdown here

Related reading on NairaSeed:

- Nigerian PAYE Tax Calculator 2026: How Much Tax Will You Actually Pay?

- How to Calculate Your Take-Home Pay in Nigeria (2026 Edition)

- NTA 2025 vs Old PITA: Are You Paying More or Less Tax in 2026?

- 6 Legal Deductions That Can Reduce Your PAYE Tax in Nigeria Right Now

Disclaimer

Tax figures in this article are estimates based on the Nigeria Tax Act 2025 as published in the Federal Government Official Gazette (June 2025). Individual tax positions vary based on employer structure, approved deductions, pensionable emoluments, and state of residence. This article is for educational purposes only and does not constitute financial or tax advice. For personalised guidance, consult a qualified tax professional or your State Internal Revenue Service.