Most Nigerian salary earners have never filed a tax return in their lives. And for a long time, that was fine. If your only income is from employment and your employer deducts PAYE correctly, you technically do not need to.

But things get more complicated the moment you earn anything outside your salary. Rental income from a property. Freelance consulting fees. Income from a side business. Dividends from an investment. Interest on a savings account above the exempt threshold. All of that is taxable, and none of it goes through your employer’s payroll.

Under the Nigeria Tax Act 2025, the rules on who must file are clear. This post explains exactly who needs to file an annual income tax return, what the process looks like, what documents you need, and what happens if you do not bother.

Who Needs to File an Annual Income Tax Return?

The short answer: not every salary earner, but more people than you think.

| Taxpayer Type | Must File Annual Return? | Deadline |

| PAYE employee with salary income only | No, if employer deducts and remits correctly | Not required |

| PAYE employee with additional income (rent, freelance, etc.) | Yes, must file to declare the extra income | 31 March each year |

| Self-employed / freelancer | Yes, always | 31 March each year |

| Business owner (sole proprietor) | Yes, always | 31 March each year |

| Employee who changed jobs during the year | Recommended, to consolidate income and correct any double-band issue | 31 March each year |

| Remote worker earning from foreign employer | Yes, income is taxable in Nigeria if you are resident | 31 March each year |

If your only income is your salary and your employer is deducting and remitting PAYE correctly every month, you are broadly covered. But the moment you have any other income source, you are responsible for declaring it yourself.

What Is the Deadline?

The annual income tax return deadline for individuals in Nigeria is 31 March of each year, covering the previous tax year. So your return for the 2025 tax year (January to December 2025) was due by 31 March 2026.

Going forward, for the 2026 tax year (January to December 2026), your filing deadline is 31 March 2027.

This is the same deadline whether you are a salaried employee filing to declare extra income or a fully self-employed individual filing your primary return.

What Documents Do You Need?

Gather these before you start. Having them ready makes the process much faster.

| Document | What It Covers | Who Needs It |

| Valid TIN (Tax ID Number) | Your unique taxpayer identifier | Everyone |

| Payslips or employer statement | Total gross income and PAYE already deducted | PAYE employees |

| Bank statements | Evidence of income received (especially for freelancers) | Self-employed, freelancers |

| Tenancy agreement and rent receipts | To support rent relief deduction claim | Anyone claiming rent relief |

| Pension statement from PFA | Total pension contributions made during the year | Everyone |

| Receipts for other deductions | NHF, NHIS, life insurance premiums | Those claiming additional deductions |

| Evidence of other income | Rental income receipts, invoices, contracts for freelance work | Those with income outside salary |

The most important item on that list is your TIN. Without a valid Tax Identification Number, you cannot file a return, and you cannot receive a Tax Clearance Certificate. If you do not have one yet, get it first. See the companion article on the Qrafteq site how to get your TIN.

How to File: Step by Step

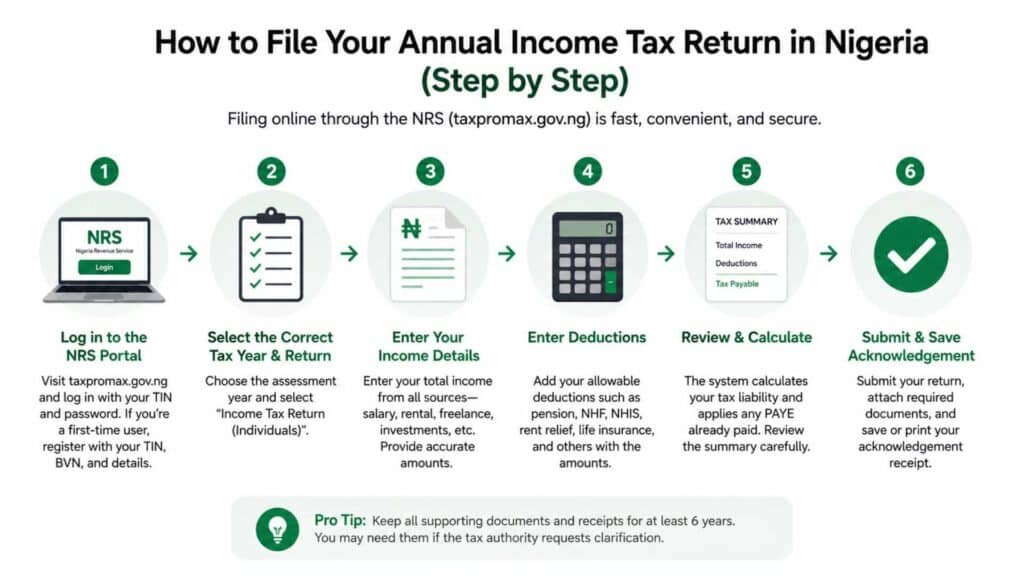

There are two ways to file in Nigeria: online through the NRS portal, or in person at your State Internal Revenue Service office. Online is faster and increasingly the standard.

Filing Online

- Visit the Nigeria Revenue Service (NRS) portal at taxpromax.gov.ng. This is the official federal tax filing platform. For state taxes, some states have their own portals, particularly Lagos (lirs.gov.ng) and Rivers State.

- Log in with your TIN and password. If you are filing for the first time, register using your TIN, BVN, and personal details.

- Select the correct tax year and click on the income tax return option for individuals.

- Enter your total income for the year. For PAYE employees with extra income, this means your gross salary from employment plus every other income source separately listed.

- Enter your deductions: pension contribution, NHF, NHIS, rent relief, life insurance, and any other approved deduction with the supporting figures.

- The system calculates your total tax liability. If your employer has already remitted PAYE on your employment income, that amount is applied as a credit. The return shows whether you owe additional tax or are entitled to a refund.

- Review everything, attach your supporting documents where required, and submit. Print or save the acknowledgement receipt.

Filing In Person

If you prefer or cannot access the online system, you can file directly at your State IRS office. Bring all your documents, ask for the individual income tax return form (sometimes called Form A), fill it in, and submit to the assessment officer. They will calculate your liability and issue an assessment notice.

In-person filing takes longer and depends on the capacity of your local SIRS office. Online is strongly recommended where available.

The Part Most Employees Get Wrong: The Double Band Problem

This catches people who changed jobs or had two income streams during the same year.

Here is the issue. When you have two separate income sources in a year, each payer (your employer, your freelance client, your tenant) treats you as if you have the full benefit of the zero-rate band on their payments alone. So two different income streams each effectively give you a N800,000 zero-rate band, when in reality you only get one per year.

The result is that your combined income is taxed at a lower effective rate than it should be across the year. When you file your annual return and declare the combined total, any shortfall in tax becomes payable.

This is not a penalty. It is just a correction to bring your total tax for the year in line with what the NTA 2025 requires on your full income. Filing the return is the mechanism that catches and corrects this.

If you had a salary job and freelance income in the same year, always file an annual return. Even if you think you do not owe anything extra, filing confirms that, and failing to file creates a compliance risk.

What Happens If You Do Not File?

| Offence | Penalty Under NTA 2025 | Notes |

| Late filing of annual return | N500,000 for individuals in some cases; interest on unpaid tax | Penalties accumulate |

| Failure to file at all | Tax authority can assess your income and charge tax plus penalties | State IRS can estimate |

| Underpayment of tax | 10% of tax due plus interest at CBN rate | Applies to shortfalls |

| No TIN registered | Cannot file or receive Tax Clearance Certificate | Get TIN first |

The practical consequence most people face is not being able to get a Tax Clearance Certificate (TCC). Banks, government contracts, property transactions, and many regulated activities require a TCC. If you have not filed your returns, you cannot get one.

Beyond that, the State IRS has the power to assess your income themselves if you do not file. They can estimate what they think you earned and raise a tax assessment based on that estimate. You then have to dispute it, which is more time-consuming and expensive than just filing in the first place.

Special Cases Worth Knowing

I am a salary earner with rental income

Rental income is taxable in Nigeria. It goes on your annual return as a separate income source. From that rental income, you can deduct expenses like repairs, maintenance, agent fees, and ground rent before arriving at the taxable amount. Keep receipts for all of these.

I do freelance work and get paid in dollars

Foreign currency income is still taxable Nigerian personal income if you are resident in Nigeria. The income is converted to naira at the exchange rate applicable at the time of receipt and declared on your annual return. Double taxation treaties between Nigeria and the country your client is based in may provide relief if that country has already taxed the income.

I earn from investments: dividends, interest, capital gains

Dividends paid by Nigerian companies typically have withholding tax deducted at source (10% under NTA 2025). This is a final tax for most purposes and does not need to be re-declared on your personal return. Interest income on most savings accounts also has withholding tax applied. However, capital gains on asset disposals (property, shares) above the N10 million exemption need to be declared. Check with a tax adviser if you have significant investment activity.

I changed jobs this year

File a return. Declare your total income from both employers across the year. The combined total will be assessed against the bands, any PAYE already remitted by both employers is credited, and any balance is settled. This is normal and the process is designed for it.

Not sure how much tax you actually owe for the year?

Use the NairaSeed Tax Calculator to estimate your full liability before you file. Enter your combined income and deductions, and the calculator shows your annual tax, effective rate, and how much of it should have already been covered by PAYE.

>> Estimate your annual tax liability here

Related reading on NairaSeed:

- How to Get Your Tax Clearance Certificate in Nigeria (2026)

- PAYE Tax in Nigeria: A Complete Guide for Employees and Employers (2026)

- 6 Legal Deductions That Can Reduce Your PAYE Tax in Nigeria Right Now

- NHF, Pension, NHIS: Which Contributions Actually Reduce Your Income Tax in Nigeria?

Disclaimer

This article is based on the Nigeria Tax Act 2025 and general tax administration practice in Nigeria as of April 2026. Tax filing procedures vary by state and may change. This article is for educational purposes only and does not constitute tax or legal advice. For personalised filing guidance, consult a qualified tax professional or your State Internal Revenue Service.