It started with one loan. Maybe a salary advance to cover rent. A quick ₦50,000 from FairMoney because something broke. A contribution you borrowed from ajo because you needed cash that week. It felt manageable then.

Then something else came up. Another loan on top of the old one. A friend you still owe from three months ago. Interest stacking every month while your salary barely covers the minimum before new expenses arrive. Now you avoid looking at your bank alert notifications because the numbers stress you out.

If that sounds familiar, you are not the only one. Personal loan rates in Nigeria range from 18% to over 36% per annum at commercial banks.

Loan apps can charge between 2.5% and 30% per month which works out to an effective annual rate running into triple digits for high-risk borrowers. Most people do not realize how fast that compounds until the debt is already bigger than their monthly income.

The only way through is a clear plan. Here is one that actually works in Nigeria.

What This Article Covers

- Why debt in Nigeria hits harder than most people expect

- How to build your full debt picture in one sitting

- Two proven repayment strategies and how to choose between them

- Where to find extra money to throw at your debt

- Why your budget is probably the real problem

- How to negotiate with lenders before things get ugly

- How to build the buffer that stops you from going back

Why Debt Hits Harder in Nigeria

Borrowing money anywhere is expensive. In Nigeria, it is particularly punishing.The CBN’s Monetary Policy Rate currently sits at 26.5%. Banks use that as their benchmark, so personal loan rates from commercial banks typically run between 18% and 28% per annum before you add processing fees and hidden charges.

Your ₦200,000 loan is not a ₦200,000 problem.Loan apps are worse. Platforms that are not CBN-licensed can charge fees that look small monthly but stack into eye-watering annual rates. And some of them, if you miss payments, have been known to send messages to people in your contact list. That is a whole different kind of pressure on top of the money stress.

Then there is inflation. Carrying debt in Nigeria while inflation eats at your purchasing power means you are losing from two directions at once. Your debt is growing. The money you repay it with is worth less. Waiting and hoping is not a strategy.

Step 1: Face the Full Picture

Most people in debt avoid looking at the total. It feels better not to know exactly how bad it is. But you cannot fix a number you have never written down.

Sit down and list every debt you owe. For each one, write the lender’s name, total amount owed, monthly repayment, and interest rate. Include everything whether it is bank loans, loan apps, salary advances, money owed to family or friends, ajo debts, credit cards. Everything.

This is your debt inventory. It will be uncomfortable to look at. That discomfort is the point. You need the full picture before any of the steps below can work.

Step 2: Stop Adding New Debt Right Now

Before you can pay anything off, you have to stop making it worse.

No new loan apps. No new salary advances. No borrowing from one person to pay another. Every new debt you take while trying to pay off old ones is like trying to bail water out of a leaking boat. You are working hard and going nowhere.

If your expenses genuinely exceed your income every month, new debt cannot fix that. It only delays the reckoning while making it more expensive. Step 5 deals with the budget problem directly. But first, close the tap.

Delete loan apps you are not actively repaying. Make it harder to borrow impulsively.

Check the FCCPC portal at fccpc.gov.ng to confirm which apps are currently approved. If an app you borrowed from is on the blacklisted list, you still owe the money but you have stronger grounds to report harassment to the FCCPC if it occurs.

Step 3: Choose a Repayment Strategy and Commit to It

There are two proven methods for attacking multiple debts. Pick one based on how your brain works, not which one sounds smarter.

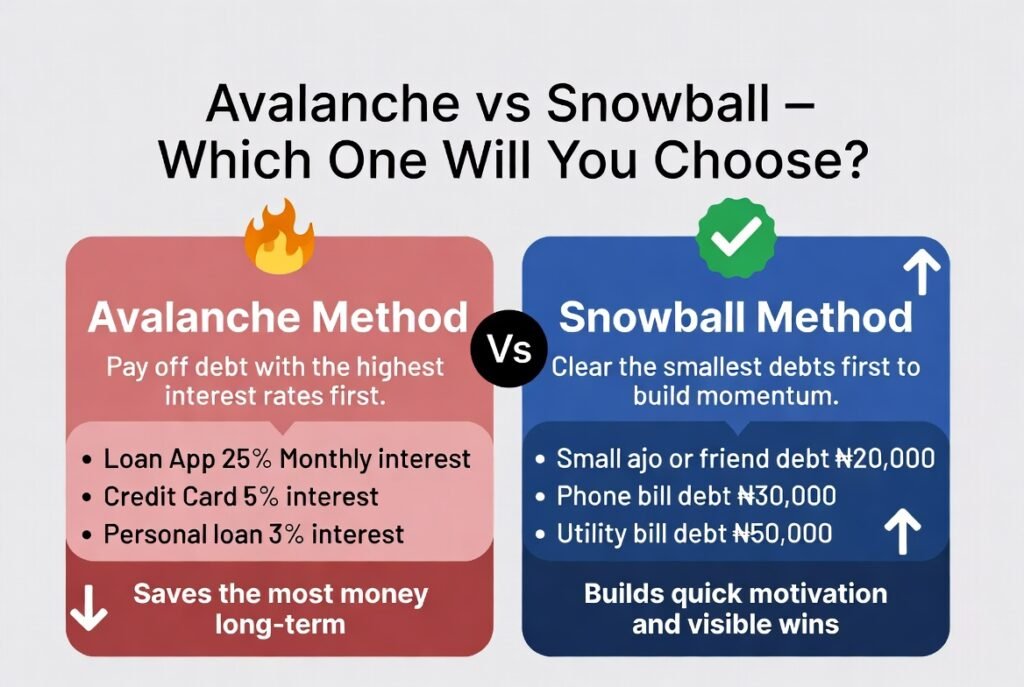

The Avalanche Method (For the Patient Person Who Hates Paying Interest)

Rank your debts from highest interest rate to lowest. Pay the minimum on every debt. Then throw every extra naira you have at the highest-rate debt first.

When that one is cleared, move to the next highest rate. Repeat.

This is mathematically the cheapest way to clear debt because you kill the most expensive debts first. But it can take a while before you feel any visible progress if your highest-rate debt is also your largest.

The Snowball Method (For the Person Who Needs to See Wins)

Rank your debts from smallest total balance to largest. Pay the minimum on every debt. Then attack the smallest balance with everything extra you have.

When it is gone, roll that entire payment into the next smallest. Each debt you clear frees up more money for the next one.

The snowball is not mathematically optimal. But it keeps people motivated because you are closing accounts and seeing real progress. A cleared debt changes how you feel about the whole process.

Neither method is wrong. The one you actually follow is the right one.

If you have one large high-interest debt and several small ones, this is also the method that protects your credit bureau record fastest because the biggest damage to your credit score usually comes from your most expensive debt running longest.

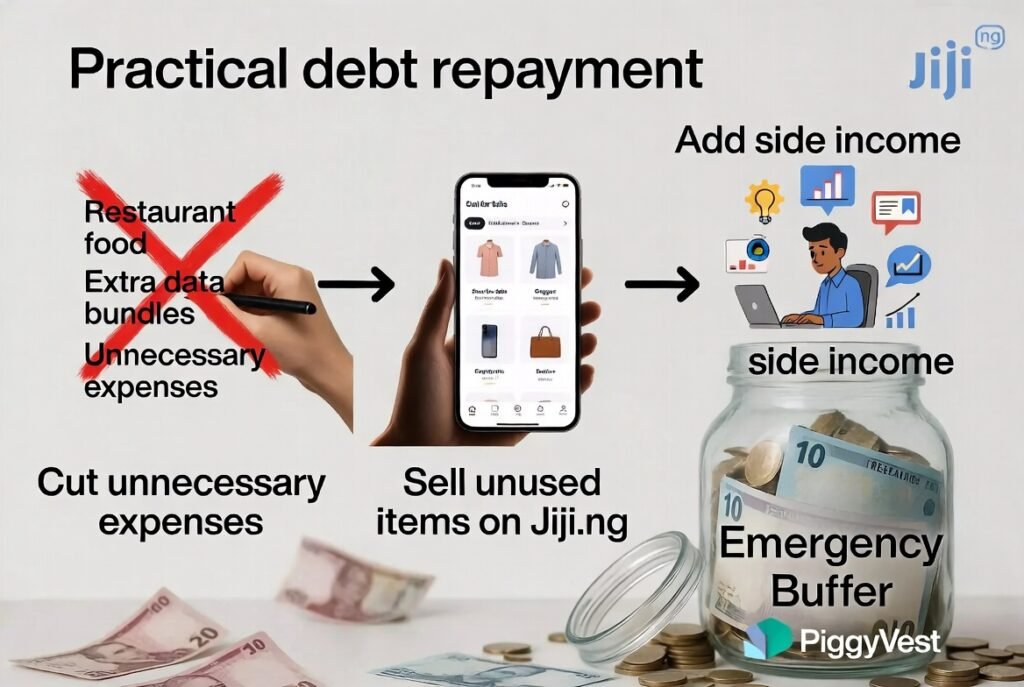

Step 4: Find Extra Money to Put Towards Your Debt

Minimum payments keep you in debt longer. You need to put more than the minimum on your priority debt every month.

Here is where Nigerians in this situation typically find it:

Cut spending that is not essential. Go through last month’s bank alerts and identify what you can pause, it could be streaming subscriptions, frequent data top-ups, restaurants. Even ₦15,000 to ₦20,000 freed up per month changes the math significantly over time.

Sell what you are not using. Clothes, old phones, gadgets, furniture. Jiji.ng and Facebook Marketplace are full of Nigerians doing exactly this every day. One solid clear-out can generate a meaningful lump sum to throw at your priority debt immediately.

Add an income stream. Freelance writing, graphic design, social media management, tutoring, data entry and so on. ₦30,000 to ₦50,000 in extra income per month reshapes your repayment timeline entirely. Fiverr and Upwork are accessible to Nigerians with marketable skills. It does not need to be a whole business. It just needs to bring in something.

Use every windfall deliberately. When a bonus arrives, when someone repays money they owe you, when a contract pays out, resist the urge to spend it. Put it straight onto your priority debt. That one decision, each time, accelerates everything.

Step 5: Fix the Budget That Put You Here

Paying off debt without changing how you spend monthly is pointless. You will be back in the same hole within a year.

A common starting framework is the 50/30/20 split: 50% of income to needs, 30% to debt repayment, 20% to savings. It is a useful anchor. But apply it to a Lagos salary and it breaks almost immediately, rent alone can swallow 40% before you buy food or pay transport.

So forget the exact percentages. The one rule that actually matters is this: spend less than you earn every month. Whatever adjustments make that happen in your specific situation are the right ones.

If your income genuinely does not cover basic needs at any split, something has to give, either an expense category shrinks or income grows. Usually both need to move.

There is no budget framework that makes ₦150,000 stretch across ₦200,000 worth of obligations. That is a structural problem, not a spreadsheet problem.

Step 6: Talk to Your Lender Before You Miss a Payment

Most Nigerians do not do this. It feels uncomfortable. Do it anyway.

If you are genuinely struggling, contact your lender before you miss a payment not after. Ask about a restructured repayment plan, an extended tenure, or a short repayment break. Banks prefer working something out to chasing a default. You lose nothing by making that call.

For loan app debt, know your rights before you panic. Debt is a civil matter, not a criminal one. Under Nigerian law, you cannot be arrested or jailed simply for being unable to repay a loan, provided there was no fraud involved in the application.

The threatening SMS messages saying your BVN will be “blacklisted” or your account frozen are often scare tactics. No private loan app can directly block or freeze your commercial bank account. Only the CBN, a court of law, or the EFCC has the legal authority to freeze an account.

What licensed lenders can do is use the Global Standing Instruction (GSI) to recover funds from other accounts linked to your BVN, and report your default to the Credit Bureau, which damages your credit score and locks you out of future loans.

That is real and it matters. But it is not jail.

For unregulated or FCCPC-blacklisted apps, and the FCCPC blacklisted 45 loan apps in Nigeria as of January 2026 for violating consumer protection and data privacy regulations, prioritise paying CBN-licensed lenders first. Regulated lenders play by rules. Unregulated ones often do not, and you have significantly less protection when dealing with them.

If you want to check what lenders have reported against your BVN, you can request your credit report from Credit Registry or CRC Credit Bureau. Every Nigerian is entitled to one free report per year. Seeing exactly what is on your credit file tells you which defaults are doing the most damage to your credit score.

Step 7: Build a Buffer So This Never Happens Again

Here is the honest reason most Nigerians end up in debt cycles: no emergency fund. When a medical bill arrived, when a car broke down, when rent came early, there was no buffer. The only option was a loan.

While you are paying off debt, start building that buffer at the same time. Even ₦5,000 to ₦10,000 a month into a locked savings account like PiggyVest SafeLock or a Cowrywise plan starts doing the job.

The goal is three months of basic expenses. Get to one month first.

This is not investment money. It is not vacation money. It is “so I never have to borrow from FairMoney again” money. That distinction matters.

The buffer does not replace the debt repayment. Both happen simultaneously. The buffer just makes sure that when life throws something at you mid-plan, you do not have to take on new debt and start over.

Practical Takeaways

- Write out every debt today: lender, amount, interest rate, monthly repayment. Total it up. You need the full number before anything else.

- Delete loan apps you are not currently repaying. Remove the easy borrowing option before you need it.

- Choose the Avalanche or Snowball method and rank your debts right now. Decision made. Move on.

- Find at least ₦15,000 extra per month to put towards your priority debt. Cut, sell, or earn it.

- If repayments are currently unmanageable, call or message your lender this week. Ask about restructuring. Do not wait until you have already missed payments.

- Open a PiggyVest or Cowrywise account and start building your emergency buffer even while repaying debt. Both problems need to be worked on at the same time.

People Also Ask

- Can you go to jail for not paying a loan app in Nigeria?

No. Loan defaulting is a civil matter under Nigerian law, not a criminal offence. You cannot be arrested simply for being unable to repay a loan, as long as you did not commit fraud during the application.

A licensed lender can pursue you in civil court as a last resort, but that is rare for small amounts. The threatening messages many loan apps send are largely illegal scare tactics.

- Can a loan app freeze my bank account or blacklist my BVN?

A private loan app cannot freeze your commercial bank account, only the CBN, a court, or the EFCC has that authority.

However, CBN-licensed lenders can use the Global Standing Instruction (GSI) to sweep funds from other accounts linked to your BVN. They can also report your default to the Credit Bureau, which lowers your credit score and affects future borrowing. Unlicensed, blacklisted apps have no legal mechanism to do either.

- Which loan apps are approved and safe in Nigeria?

As of 2026, the FCCPC has blacklisted over 45 loan apps for violating consumer protection and data privacy rules. Safe, regulated options include CBN-licensed platforms like Carbon, FairMoney, and Branch.

Before borrowing from any app, verify it on the CBN website at cbn.gov.ng and the FCCPC portal at fccpc.gov.ng. If an app is not listed on either, avoid it.

- What is the difference between the Avalanche and Snowball debt repayment methods?

The Avalanche method targets your highest-interest debt first, which saves the most money in the long run.

The Snowball method targets your smallest balance first, which creates visible wins faster and keeps you motivated.

Both works, the right one is whichever you will actually stick to.

- Does loan default affect my credit score in Nigeria?

Yes. Licensed lenders report defaults to Nigeria’s Credit Bureaus, CreditRegistry and CRC Credit Bureau are the main ones.

A default on your credit report makes it harder to get future loans from banks, microfinance institutions, and regulated loan apps. Clearing the debt and maintaining a clean repayment record over time gradually rebuilds your score.

- What is debt consolidation and does it work in Nigeria?

Debt consolidation means taking one larger loan at a lower interest rate to pay off multiple smaller, higher-rate debts leaving you with one monthly payment instead of several.

Some Nigerian banks and microfinance institutions offer this. It works best when you can genuinely access a lower rate than what you are currently paying, and only if you stop accumulating new debt after consolidating. Without fixing the spending pattern, consolidation just resets the clock.

Final Word

Here is what this plan actually requires: a written list, a decision on one repayment method, and more money going to debt this month than last month. That is it.

You do not need a windfall. You do not need to earn more before you start. You need the full number in front of you and a direction to walk in.

Most people who get out of debt in Nigeria do not do it because their circumstances changed dramatically.

They do it because they stopped avoiding the number and started attacking it with whatever was available, ₦10,000 here, a sold item there, a renegotiated repayment elsewhere.Write the list today.

The rest follows from that.

Sources: CBN Monetary Policy Rate – Central Bank of Nigeria | GSI policy and loan app account freezing – Nigeria Housing Market | FCCPC blacklisted loan apps 2026 – Legit.ng | Loan default as civil matter – Nairametrics

Related: PiggyVest vs Cowrywise vs Risevest: Which One Should You Be Using in 2026? | How to Build a 6-Month Emergency Fund in Nigeria