If you have any money saved right now, even ₦50,000 sitting in an account, someone in your life has an opinion about what you should do with it. Your friend in Canada says keep everything in dollars. And while your dad says put it in land, the finance Twitter people on the other hand, say T-bills. Your bank’s app is sending you notifications about a “high-yield savings plan” that pays 6% while inflation is running at 15%.

Dollar vs naira savings in 2026 is not a simple question. But most of the answers people are giving you are too simple. This post tries to fix that.

Table of Contents

- Where the naira actually stands in 2026

- The quiet way naira savings lose your money

- What dollars actually do for you — and what they don’t

- Dollar vs naira savings: the honest side-by-side

- Where to keep your money based on what you’re saving for

- Action steps for this week

1. Where the naira actually stands in 2026

IMAGE: Naira and dollar notes

Nobody who watched 2023 and 2024 is walking around with full confidence in the naira. That is just honesty. The CBN’s decision to float the exchange rate properly sent the official rate tumbling, the parallel market moved even faster, and anyone with naira savings watched their purchasing power shrink in a way that felt almost personal.

2026 is calmer. The gap between the official and parallel market rates has narrowed. The CBN has more foreign reserves than it did two years ago. Nigeria’s inflation dropped to 15.06% in February 2026 according to the National Bureau of Statistics, which sounds like progress until you remember it was 26.27% the same time last year and 15% is still not low.

The naira is not fixed. It is stabilised, at least for now. Those are two different things, and the difference matters for how you think about where to keep your money.

The bank recapitalisation that wrapped up on 31 March 2026 (where 33 banks raised a combined ₦4.65 trillion to meet the CBN’s new capital requirements) adds one more layer to this. Stronger banks are now competing for your deposits in a way they weren’t before. Some are offering better fixed deposit rates. Some are launching new savings products. Whether that actually beats inflation is a separate question, and we’ll get to it.

The full breakdown of what recapitalisation means for your finances is here: What the Completed Bank Recapitalization Means for Your Savings, Loans, and Investments in 2026.

2. The quiet way naira savings lose your money

Here is the part most people skip past because the maths feels abstract.

If you have ₦1 million in a standard savings account paying 4% per year, you end 2026 with ₦1,040,000. That looks fine on paper. But if inflation runs at 15%, you need roughly ₦1,150,000 at the end of the year to buy what ₦1 million bought at the start of it. You didn’t save. You just lost money more slowly than if you’d kept it under your mattress.

This is not an argument against naira savings. It is, on the contrary, an argument against lazy naira savings, putting money in the first account your bank opened for you and leaving it there because moving it feels like too much work.

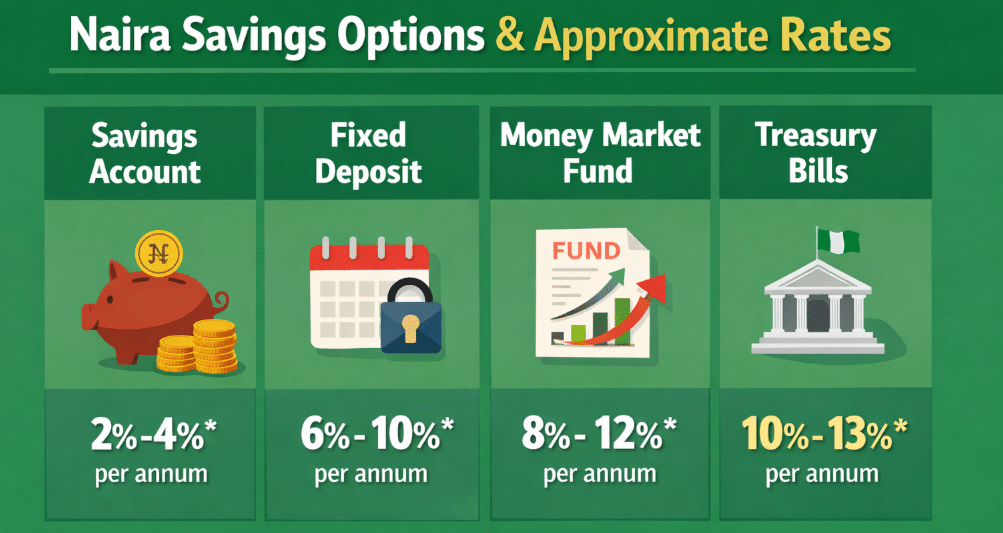

The naira products that actually make sense in 2026:

Treasury bills. The CBN has been running T-bill auctions at rates that have crossed 20% at points this year. For money you will not need for 91 days or more, this is the strongest low-risk naira option on the table right now. You can access it through your bank’s investment desk or through platforms like Cowrywise and PiggyVest.

Fixed deposits at recapitalised banks. Some of the larger banks are now offering between 15% and 18% on 90-day to 180-day fixed deposits as they compete for retail deposits post-recap. That is not guaranteed to beat inflation, but it is significantly better than a standard savings account. This is serious business, so to go about this, call your bank’s investment desk, not the regular customer service line — and ask specifically what their current fixed deposit rates are.

High-yield savings platforms. PiggyVest, Cowrywise, and Risevest are regulated, have been operating long enough to have a real track record, and typically beat standard bank savings rates. Check the current rates before you commit, because they change too.

IMAGE: Graphic comparing naira savings options and approximate rates

3. What dollars actually do for you (And what they don’t)

Dollars do one thing really well: they hold value when the naira is under pressure. If the naira falls again (and at some point in the next few years, there will be pressure, that is just Nigeria’s reality), dollar savings protect you against the worst of it. But for payment for school fees abroad, medical bills that end up in foreign currency, importing goods for your business, dollar savings make those things less painful.

What dollars do not do is grow on their own.

A domiciliary account at a Nigerian bank pays somewhere between 0% and 1% annually on dollar deposits. That means ₦2 million converted to roughly $1,250 at today’s rates, sitting in a domiciliary account for a year, earns you about $12. The dollars are safe. They are not working.

If you want dollar savings to actually grow, you need to be using a dollar-denominated investment product — platforms like Bamboo, Risevest’s dollar plans, or Eurobonds through a licensed stockbroker. These carry their own risks and you should read the terms properly before putting money in. But if you are converting naira to dollars and leaving it in a bank account doing nothing, you have solved one problem and created another.

The other thing dollars don’t give you is easy access in a naira emergency. Converting back takes time. There is always a spread, such that the rate you sell at is never the rate you see quoted. If your emergency fund is sitting entirely in dollars and something happens at 10pm on a Friday, you are going to have a bad weekend.

4. Dollar vs naira savings in 2026: the honest side-by-side

| What You Are Weighing | Naira Savings (2026) | Dollar Savings (2026) |

|---|---|---|

| Inflation protection | Weak in standard accounts; better in T-bills and fixed deposits | Strong if naira falls; neutral if it holds steady |

| Growth potential | 15%–20% possible in T-bills and fixed deposits | Near zero in domiciliary accounts; 5%–10% in dollar investment products |

| Access when you need it | High — easy to move and spend | Lower — conversion takes time and costs money |

| Main risk | Inflation and potential naira pressure | Exchange rate locks, platform risk on investment products |

| Best suited for | Emergency funds, naira-priced goals, short-term savings | International goals, school fees, long-term wealth diversification |

| Where to put it in 2026 | 90-day T-bills or fixed deposits for idle cash | Regulated dollar investment platforms for medium to long-term goals |

5. Where to keep your money based on what you’re saving for

The mistake most people make is picking a currency based on how they feel about the naira right now, rather than thinking about what the money is actually supposed to do.

Your emergency fund — naira, accessible, earning something. This money needs to be reachable fast. A high-yield savings account on PiggyVest or a short-tenure fixed deposit at your bank is the right home for it. Three to six months of your expenses, in naira, somewhere you can get to it within 24 to 48 hours. Do not put your emergency fund in dollars. The conversion friction will cost you at the worst possible moment.

Saving for something priced in naira — stay in naira, but do it properly. Rent. A car. Business stock. Equipment. Whatever the goal is, if you will pay for it in naira, save for it in naira instruments — T-bills, fixed deposits, or a regulated savings platform. The goal is to beat or at least match inflation while you wait. A standard savings account at 4% will not do that.

Saving for something priced in foreign currency — start in dollars from day one. School fees abroad, a trip, equipment you will import. The moment you know a goal is denominated in foreign currency, start saving in that currency. Converting naira to dollars at the last minute — when you actually need the money — is one of the most reliable ways to get a bad rate. The people who do well here are the ones who decided early and converted gradually.

Long-term wealth building — both, deliberately. Nigerian stocks, real estate, and T-bills on the naira side. Dollar investment platforms and Eurobonds on the dollar side. The split depends on your income, your goals, and how much naira risk you can tolerate. There is no universal answer. Anyone who tells you there is a specific percentage — “keep 70% in dollars” — without knowing your situation is guessing.

6. Action steps for this week

- Find out what your savings account is actually paying you right now. Log into your banking app or call your bank. If it is below 10%, your money is losing real value.

- Check the current 91-day Treasury bill stop rate on the CBN website. That number is your naira benchmark — anything earning less than that is costing you.

- If you do not have a domiciliary account, open one this week. You do not need to put money in it yet — just have it ready before you need it.

- Write down what each of your savings pools is actually for, and which currency that goal will be paid in. That exercise alone will tell you where to keep each one.

- If you have dollar savings sitting idle in a domiciliary account, spend 30 minutes this week looking at one regulated dollar investment platform. Bamboo, Risevest, and Trove are starting points — read the current rates and the withdrawal terms before you do anything.

The naira has real problems. The dollar is not a magic fix. In 2026, the people who are doing well on both sides are not the ones who picked the right currency — they are the ones who matched their savings to what the money was actually for.

Got a specific savings situation you want a straight opinion on? Drop it in the comments.

If you run a small business and you are wondering what the recapitalisation means for your loan options, read What Bank Recapitalization Means for Nigerian SMEs: Easier Loans, More Grants, or Just Hype?. For the full picture on how the recap affects savings, bank stocks, and investments, start with What the Completed Bank Recapitalization Means for Your Savings, Loans, and Investments in 2026.

Money wisdom, planted in Africa.